Last updated: March 11, 2026 • Author: Effortless Mortgage

Mortgage refinancing isn’t just about rates — it’s often about making your monthly budget easier. Whether you’re a homeowner or a homebuyer, this is worth knowing: refinancing is simply updating your mortgage plan to better fit your life today.

And if you’re a first-time buyer, don’t worry — you don’t need to “know refinancing” yet… but understanding it now will help you plan smarter later.

Here’s the big misconception we hear all the time: “Refinancing only makes sense if rates drop a lot.” Not always.

Because refinancing isn’t just about rates. A lot of the time, it’s about making your monthly budget easier.

TL;DR

TL;DR:

-

Refinancing isn’t only a rate play — it can be a monthly budget / cash flow move.

-

Homeowners refinance for two big reasons: (1) reduce monthly pressure and (2) access home equity for a purpose.

-

If you want to access equity, your home appraisal matters — and appraisals can come in lower than expected compared to a couple years ago.

-

Even without taking a big lump sum out, refinancing can still help when the goal is simplifying payments.

-

Real example below shows $4,294/mo → $2,367/mo.

What Refinancing Means

Refinancing means you’re changing your current mortgage. That can involve:

- adjusting your rate or term

- changing your payment structure

- consolidating other debts

- accessing equity (if it fits your plan)

Why People Refinance

1) To lower the pressure on monthly payments

This is one of the most common reasons right now.

If you have multiple high-interest payments (credit cards, lines of credit, etc.), refinancing can sometimes combine things into one payment that’s easier to manage.

2) To access equity for something specific

Examples:

- home renovations

- buyout / separation

- investing in a property

- tuition payments

- a major life change where a cash buffer helps

Quick Heads-Up: Appraisals Matter

If you’re trying to access equity, your home’s appraisal matters a lot — and appraisals can come in lower than people expect compared to a couple years ago. That can limit how much you can take out.

But even when you’re not taking out a big lump sum, refinancing can still help if the goal is simplifying payments and improving monthly cash flow.

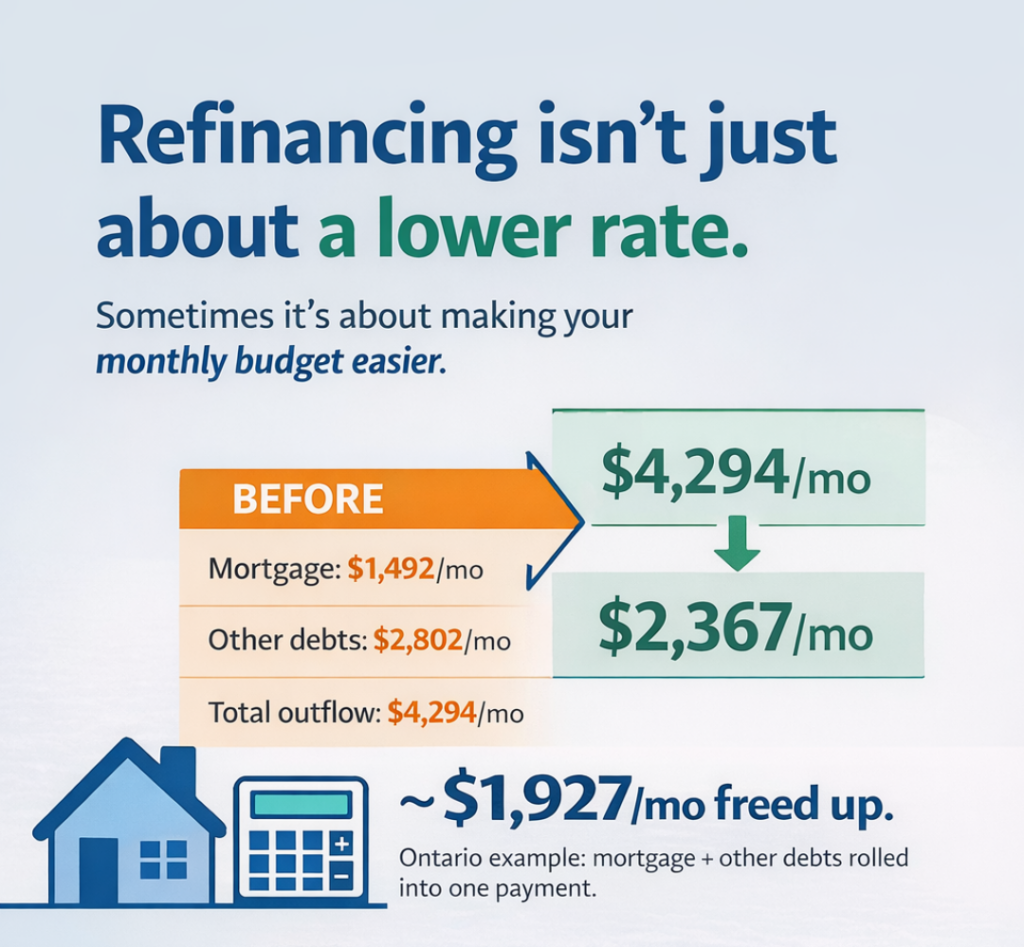

A Real Mortgage Refinancing Example (with actual numbers)

Here’s a real-life style example we see often:

Before

👉 Current mortgage balance: $305,000

👉 Current mortgage payment: $1,492/month

👉 Other monthly debt payments (cards/LOC/vehicle/etc.): $2,802/month

That’s $4,294/month going out the door.

After refinancing (rolling debts into the mortgage):

✅ New mortgage balance: $470,000

✅ New all-in monthly payment: $2,367/month

That’s a drop from $4,294 → $2,367/month

= $1,927/month freed up in cash flow.

Not because of a “magic rate” — but because they stopped paying high interest in multiple places and simplified everything into one plan.

When Refinancing Usually Makes Sense

Refinancing is worth exploring when:

-

your mortgage + other debt payments are stacking up

-

you want to consolidate high-interest debt into one payment

-

you need equity for a clear purpose (reno, buyout, investing)

-

your current mortgage no longer fits your life

It may not be worth it when:

-

you’re only chasing a tiny rate drop and the savings are minimal

-

penalties/fees outweigh the benefit based on your timeline

-

you plan to sell soon (timing matters)

What We Look at When We "Run the Numbers"

To tell you if refinancing makes sense, we look at:

- your current mortgage details (rate, term, renewal date)

- any penalty to break early (if applicable)

- your home’s estimated value + what an appraisal might support

- your full debt picture (this is often where the biggest monthly relief is)

- your timeline and goals

We’ll explain it in plain language so you can decide without guessing.

FAQs

We keep this page updated so you can check current mortgage rates Canada without hunting across multiple sites.

Will checking refinance options affect my credit score?

Not just by asking questions. If we need a credit check for an application, we’ll tell you first.

Can I refinance if my home value isn't what it was in 2021-2022?

Sometimes yes, sometimes no — it depends on equity, income, credit, and the goal. If equity access is limited, payment restructuring may still be an option.

Is refinancing only for people who want cash out?

No. Many refinances are done to simplify payments and reduce monthly pressure.

What costs are involved?

Potential costs can include mortgage break penalties (if mid-term), appraisal/legal fees, and lender fees depending on the lender. We’ll show you the math so you can decide if it’s worth it.

What if refinancing isn't possible right now?

You may still have options depending on your equity and goals. We’ll review what fits (and what doesn’t) so you can make a clear decision.

Ready to Explore Your Options?

Contact Effortless Mortgage today to get connected with trusted private lenders Ontario homeowners rely on.

We have VIP relationships with over 90+ banks, b lenders and private mortgage lenders including our own in-house private lender with $0 broker fee.

Call us at 1-888-978-4984

Call us at 1-888-978-4984 Email info@effortlessmortgage.ca

Email info@effortlessmortgage.ca