Featured Rate Today: 3.30%

- Featured starting rate: 3.30%

- Best fit for: borrowers with strong qualifications (details matter).

Check if you qualify for 3.30%. Use the QUOTE FORM on this page (takes ~2 minutes). We’ll confirm what you qualify for and show the best-fit options.

Check if you qualify for 3.30%. Use the QUOTE FORM on this page (takes ~2 minutes). We’ll confirm what you qualify for and show the best-fit options.

Prefer to speak to a human first? Book a quick 15-minute call.

*Important disclosure: 3.30% is a starting rate for select scenarios, subject to change and approval. Final rate depends on credit, down payment/equity, income, property, and lender program.

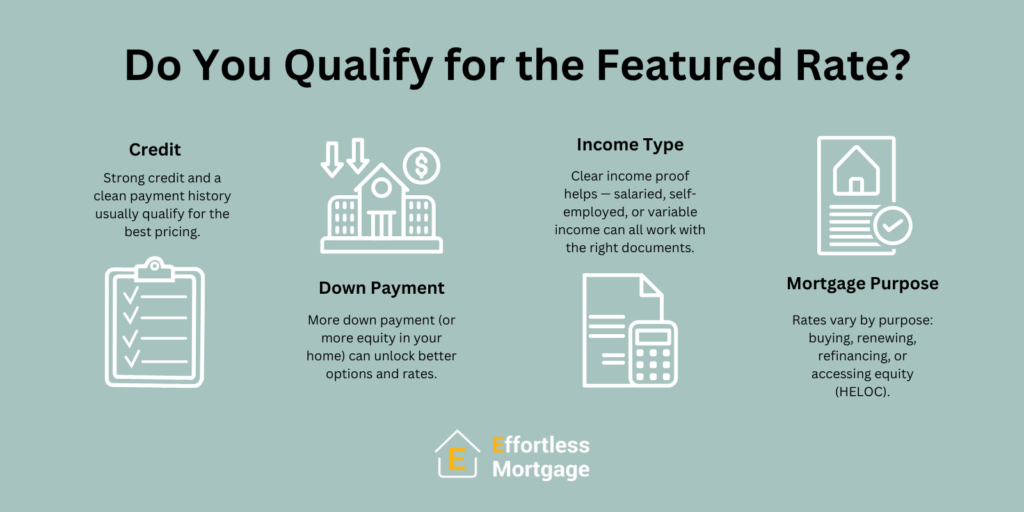

Who this featured rate is usually best for…

This featured rate may be a good match if:

you have strong credit and solid repayment history

you have strong credit and solid repayment history

your income and documents are straightforward (or well-prepared if self-employed)

the property and mortgage request fits the specific lender criteria

you’re comfortable with the term/type that comes with that rate

Not sure? That’s normal. Use the quote form and we’ll tell you quickly if it fits — and what the best alternatives are if it doesn’t.

Contact Effortless Mortgage today to get connected with trusted private lenders Ontario homeowners rely on.

We have VIP relationships with over 90+ banks, b lenders and private mortgage lenders including our own in-house private lender with $0 broker fee.

Call us at 1-888-978-4984

Call us at 1-888-978-4984 Email info@effortlessmortgage.ca

Email info@effortlessmortgage.ca