What You Need to Know to Prove the Source of Your Down Payment (for Home Buyers)

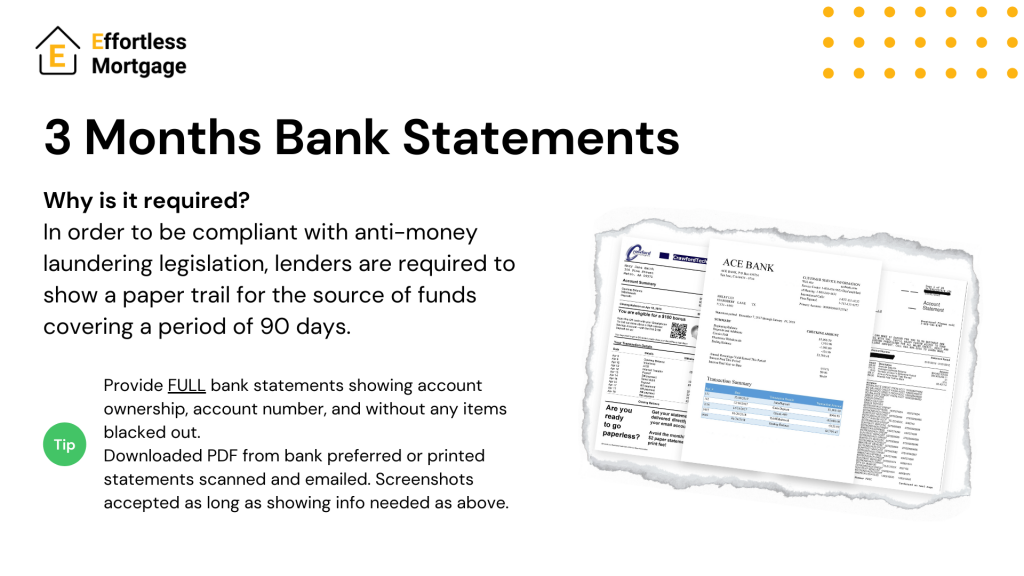

First off, it is important to know that, due to the anti-money laundering legislation, all lenders are required to show a paper trail for the source of down payment covering a period of 90 days.

Second, it is important to know that proving the source of down payment to purchase a home can be a very stressful part of the mortgage journey … or, it can be a piece of cake.

The difference is in how prepared you are.

We are going to help you get prepared, so you don’t worry and this part of the mortgage journey will be a piece of cake.

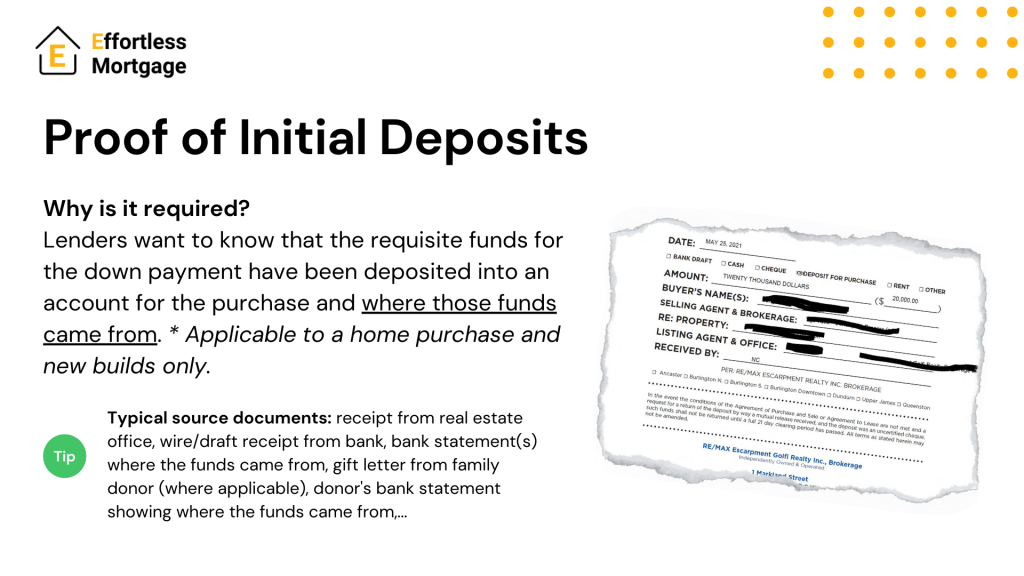

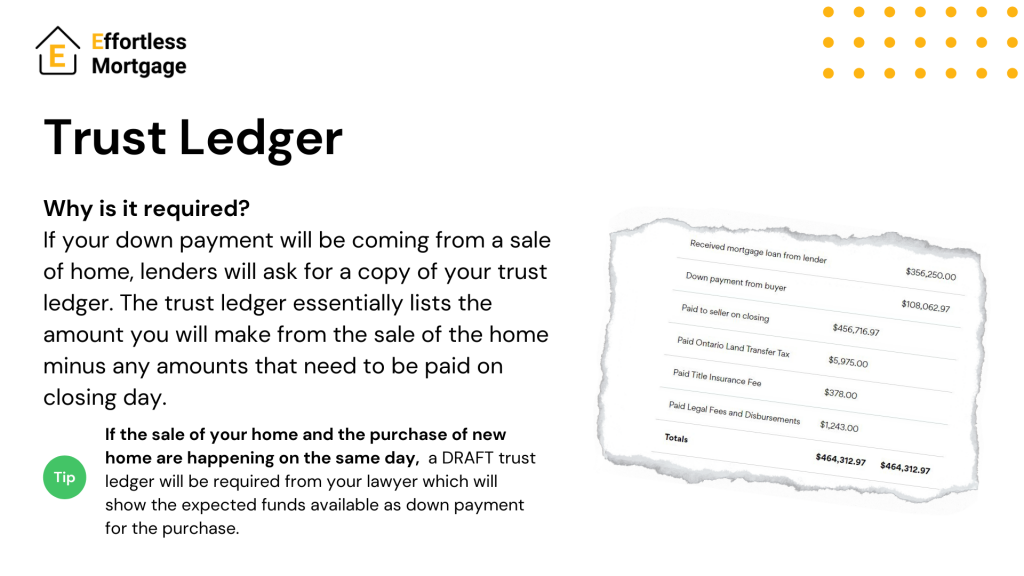

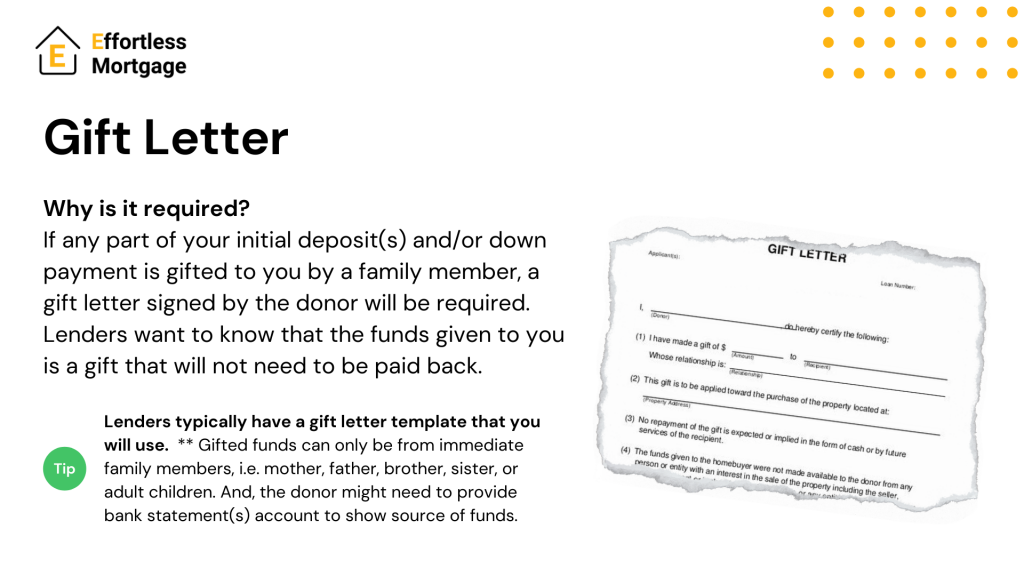

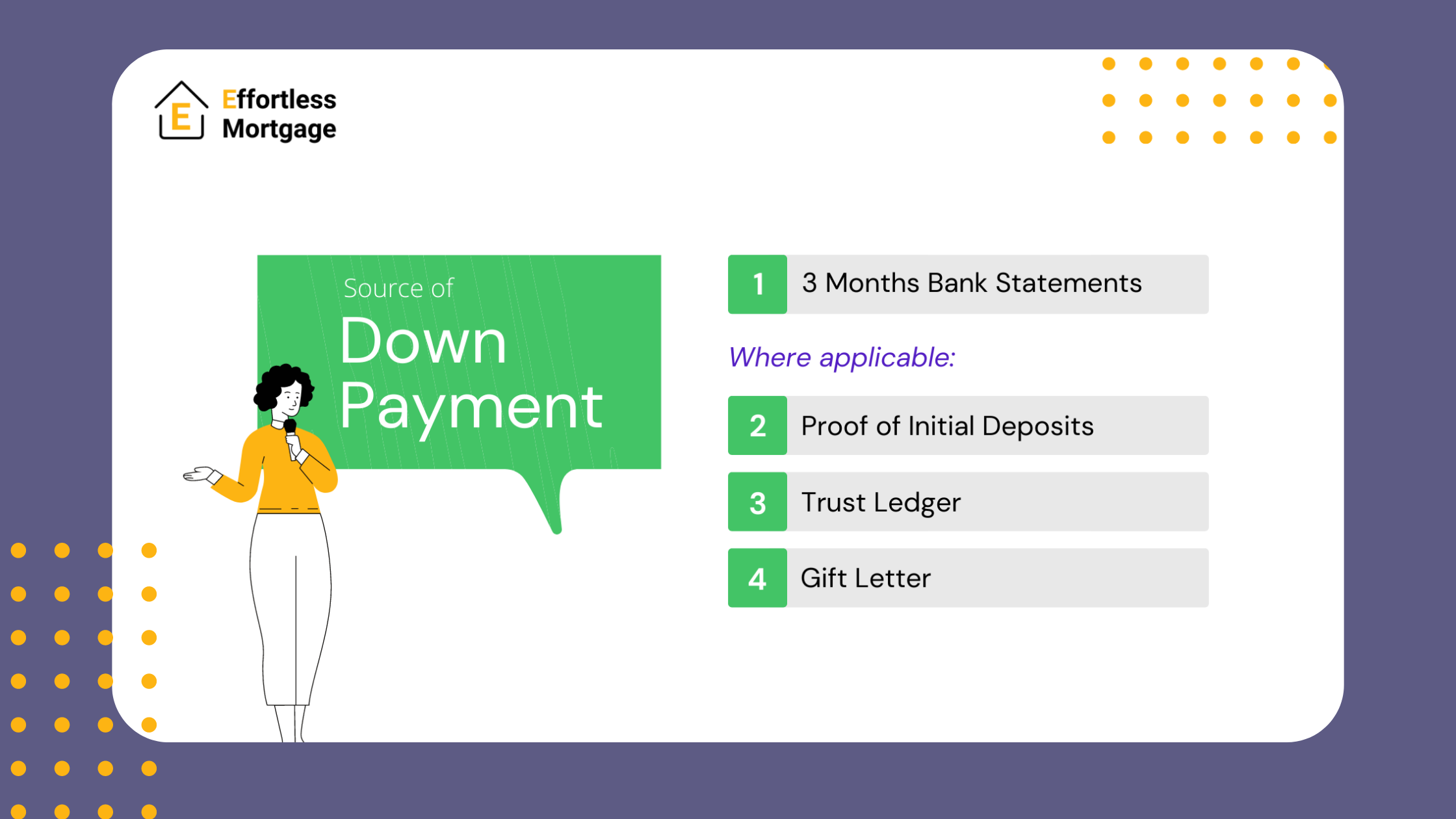

Proving the source of your down payment really means that you have to show exactly where the money for your down payment is coming from, i.e. cash gift from a family member, investments, savings, RRSPs, sale of a home, etc.

Once your offer has been accepted, the mortgage lender will have “outstanding conditions” for you and your broker to satisfy including proving and sourcing your down payment.

By having a better understanding of what the lender will be looking for, as well as the reasoning, the process will be much easier and faster.

Below are the FOUR typical sources of down payment most lenders will ask for.