Last updated: May 30, 2026 • Author: Effortless Mortgage

Who needs a private mortgage in Ontario?

Most people assume a private mortgage is only for someone in a worst-case situation.

That’s not always true.

In Ontario, a private mortgage may come into the picture when someone does not neatly fit a bank’s lending guidelines right now — even if they have income, equity, or a plan to improve their situation.

In many cases, it is not about being out of options. It is about needing a different type of mortgage solution for a period of time.

TL;DR

TL;DR:

-

A private mortgage is not always for someone in major financial trouble.

-

It may come into the picture for self-employed borrowers, bruised credit, high debt ratios, urgent closings, or people recovering from past credit issues.

-

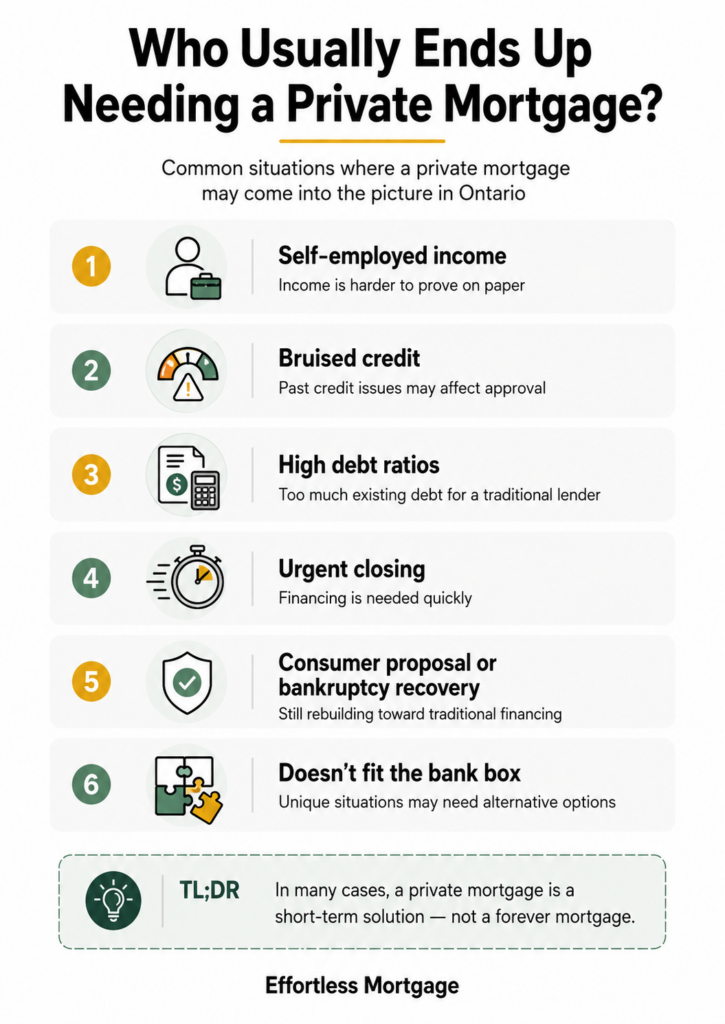

In many cases, a private mortgage is a short-term solution, not a forever mortgage.

-

The key is understanding the costs, risks, and exit plan before moving forward.

What is a Private Mortgage in Simple Terms?

A private mortgage is a mortgage funded by a private lender instead of a traditional bank or major institutional lender.

That does not automatically mean it is the wrong choice. But it does mean the mortgage should be looked at carefully.

Private mortgages often come with:

- higher interest rates

- lender or broker fees

- shorter terms

- a need for a clear exit strategy

That is why they are often used as a temporary solution while a borrower works toward qualifying for a better long-term mortgage later.

Who Needs a Private Mortgage in Ontario?

Here are some of the most common situations where a private mortgage may come into the picture in Ontario.

1) Self-employed borrowers with hard-to-prove income

A lot of self-employed people earn good money, but their tax returns may not tell the full story.

Maybe they write off a lot of expenses.

Maybe their income looks inconsistent on paper.

Maybe they have only been self-employed for a short time.

Even when the borrower is financially capable, a bank may not feel comfortable with how the income looks.

That is one reason a private mortgage may be considered.

2) People with bruised credit

Some borrowers hit a rough patch.

That could include:

- missed payments

- collections

- a low credit score

- past credit mistakes that are still affecting mortgage approval

It does not always mean they are financially reckless now. Sometimes it means they are still recovering from a difficult period and need time to rebuild.

A private mortgage may help bridge that gap.

3) Borrowers with high debt ratios

Sometimes the issue is not income alone. It is the amount of debt a borrower is already carrying.

For example:

- high credit card balances

- personal loans

- car loans

- lines of credit

- other monthly obligations pushing ratios too high

A traditional lender may decline the application, even if the borrower feels they can manage the payment.

In some cases, a private mortgage is used while the borrower works on reducing debt or restructuring their finances.

4) Buyers facing an urgent closing

Timing matters in mortgages.

Sometimes a borrower needs financing fast and does not have time for the back-and-forth that can come with a traditional lender.

That might happen with:

- a firm purchase closing date

- delays in paperwork

- income documents that need more explanation

- a deal that needs to close before other financing can be arranged

A private mortgage can sometimes help keep the purchase alive when timing is tight.

5) People coming out of a consumer proposal, bankruptcy, or other credit issues

Some borrowers are on the way back financially, but they are not quite where a traditional lender wants them to be yet.

They may have:

- completed a consumer proposal

- gone through bankruptcy recovery

- rebuilt some credit, but not enough

- stabilized income but still need more time

This is another situation where a private mortgage may be used as a stepping stone, not an end goal.

6) Borrowers who do not fit the bank’s box right now

This is often the biggest one.

A borrower may have:

- a unique property

- non-traditional income

- a complicated financial picture

- recent life changes

- a file that makes sense in real life, but not neatly on paper

Banks rely on guidelines. If the file does not fit those guidelines, the answer may be no — even when the situation may still be workable.

That is where private lending may come into the conversation.

Does Needing a Private Mortgage Mean You are Out of Options?

No.

It may simply mean that traditional financing is not the right fit right now.

That is an important difference.

A private mortgage is often used as a way to:

- buy time

- complete a purchase

- deal with short-term credit or debt issues

- create a path back to a better mortgage later

The goal should usually be to understand:

- why the private mortgage is needed

- what it will cost

- how long it is expected to be used

- what the plan is to exit it

What Should You Watch Out For With a Private Mortgage?

A private mortgage can be useful in the right situation, but it should never be approached casually.

Borrowers should clearly understand:

- the interest rate

- fees involved

- the term length

- payment expectations

- the exit strategy

The biggest mistake is focusing only on getting approved and not thinking about what happens next.

FAQs

Who needs a private mortgage in Ontario?

Private mortgages may be used by self-employed borrowers, people with bruised credit, high debt ratios, urgent closings, or borrowers recovering from credit challenges.

Is a private mortgage only for bad credit?

No. Bad credit is one reason, but private mortgages may also be used by borrowers with non-traditional income, time-sensitive closings, or situations that do not fit a bank’s guidelines.

Is a private mortgage a long-term solution?

Usually not. In many cases, a private mortgage is meant to be a short-term option while the borrower works toward qualifying for a better long-term mortgage

Can self-employed people get a private mortgage?

Yes. A private mortgage may be an option for self-employed borrowers whose income is strong in real life but harder to prove in the way traditional lenders require.

Ready to Explore Your Options?

If your situation feels outside the usual bank box, it is worth asking questions before assuming you have no options.

Contact Effortless Mortgage today to get connected with trusted private lenders Ontario homeowners rely on.

We have VIP relationships with over 90+ banks, b lenders and private mortgage lenders including our own in-house private lender with $0 broker fee.

Call us at 1-888-978-4984

Call us at 1-888-978-4984 Email info@effortlessmortgage.ca

Email info@effortlessmortgage.ca